The Most Critical Investment Decision

Doc's note: You don't need a professional to manage your portfolio for you. According to my good friend and Stansberry Research founder, Porter Stansberry, portfolio management is the surest way to boost your results.

But in today's issue – adapted from a March issue of The Big Secret on Wall Street, published by his firm Porter & Co. – Porter shares four critical concepts to help you manage your portfolio, improve its performance over the long term, and avoid big losses...

![]()

George Maddox went "all in" on one stock with his retirement savings... and it almost worked out for him.

George had played by the rules and done just about everything right.

For more than 30 years, he had been a loyal, hardworking employee at what was one of America's largest companies. He scrimped and saved, putting money into his employee stock plan every month. And by the time he retired, he owned more than 14,000 shares – a holding that was eventually worth well over $1 million.

George was set for life... or so he thought.

Unfortunately, George's former employer was Enron.

When the now-notorious energy-trading firm went bankrupt following massive accounting fraud in 2001, its stock price cratered from more than $90 per share to just 26 cents... and George's nest egg collapsed in value to just $3,600.

Lou Pai – who was the head of Enron's Energy Services division in Houston – likely would have been in a similar position to George.

Like George, Lou had virtually all of his (significantly larger) net worth invested in Enron stock. But he had developed an obsession with Houston's high-end strip clubs... This obsession led to his divorce and he was forced to sell his Enron shares – before the accounting scandal erupted in 2001. So when the company folded not long after, and the stock plunged, Lou's $280 million net worth was safely not invested in Enron shares.

What ultimately separated George and Lou – besides dumb luck – was one of the simplest yet most important concepts in investing...

Asset allocation – how investors invest, or "allocate," their capital across (and within) different asset classes like stocks, bonds, real estate, and commodities – is critical.

Research suggests that asset allocation can play a more important role in investors' long-term success than which individual investments they own. Various studies have shown that the specific combination of assets in a portfolio explains between 80% and 94% of its total return.

However, proper asset allocation is also a highly individual matter. No one-size-fits-all allocation is appropriate for every investor in every situation.

One popular asset allocation model is the "60/40 portfolio" – consisting of a 60% allocation to stocks and a 40% allocation to bonds or fixed income. Another popular approach is the "100 minus your age" rule, which designates a gradually smaller percentage to stocks (and therefore, a larger percentage to bonds) as an investor grows older.

There are virtually endless ways to invest across various asset classes depending on personal circumstances. And we simply can't provide the kind of individualized advice that would be required to make those decisions on your behalf.

That said, earlier this year, Porter & Co. Biotech Frontiers analyst Erez Kalir joined me for an in-depth discussion on this topic.

And today, I'm sharing some key highlights from our talk...

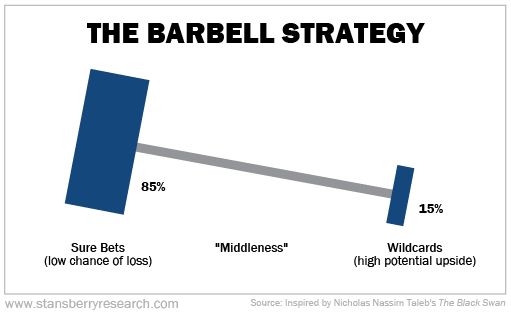

1. Balance Your "Risk Barbell"

Think of an investment portfolio as a barbell. The goal is to offset any high-risk assets on one side with super-safe assets on the other, so that overall portfolio risk is balanced.

The Big Secret on Wall Street subscribersknow we believe investors don't need to take a lot of risk to earn market-beating returns over the long run.

But this rule implies that if an investor does decide to invest in riskier assets, he must take care to own super-safe and prudent investments as well. And generally, the more risk an investor takes on one side, the more conservative he should be on the other.

This idea also encourages sensible position sizing, helping to ensure an investor doesn't invest too much capital into any one position.

2. Know Your Investment Horizon and Risk Tolerance

A second critical idea is the importance of knowing your investment horizon and risk tolerance.

"Forever" stocks are stocks you can buy and hold forever... The surest way to build wealth in the market is to simply buy great businesses when they trade at good prices and never sell them – allowing the magic of compounding to multiply your capital tax-free.

But holding an investment for decades isn't practical for every investor. Depending on one's age and personal circumstances, an individual's investment horizon may be far shorter. And this should play a significant role in their asset-allocation decisions.

For example, investors with a shorter investment horizon – if they need a specific amount of money for a home purchase or retirement, for example – would generally be well served to allocate a greater percentage of their portfolios to fixed-income investments and less to equities.

Similarly, risk tolerance should heavily factor into an investor's allocation decisions.

For example, even Warren Buffett's Berkshire Hathaway – one of the greatest businesses in history and an extraordinarily low-risk stock – has temporarily lost 50% of its value on three separate occasions over the years before rebounding to new highs.

Investors who can't tolerate that type of volatility would be wise to minimize their equity exposure as well and focus more on lower-volatility fixed-income opportunities.

3. Maintain a Reasonable Number of Positions

This idea should be relatively obvious – but is often overlooked. Even full-time or professional investors only have so much time and mental bandwidth to devote to each investment position.

Yet it's not uncommon for many investors to end up owning dozens, or even hundreds, of individual positions. This is a recipe for poor returns if not outright disaster.

Erez and I agree that most investors should limit the total number of individual investments to no more than 18 positions. This is a small enough number to be manageable for most investors, while still allowing for a good amount of diversification.

The one major exception to this rule would be broad-market or broad-asset exposure held through mutual funds or exchange-traded funds ("ETFs") that don't necessarily require the same degree of oversight.

4. Embrace Change With "Dynamic Allocation"

Markets – like the seasons – change. Some assets, sectors, and individual companies come into favor, while others fall out of favor. Some become wildly overvalued, while others are left for dead.

Investors who are willing to occasionally "break the rules" and allocate significant portions of their portfolios to extreme value can earn incredible returns with very little risk.

This approach was a favorite of the late Berkshire vice chair and Buffett sidekick Charlie Munger, who passed away late last year.

Investors would routinely ask Munger how to get rich in stocks, and he would consistently point to these kinds of rare opportunities – opportunities that may only come along a handful of times in an investor's entire lifetime.

The key, Munger noted, was to have the patience to wait for these "fat pitches" to come along... and then to have the courage to "swing hard" when they inevitably arrive.

Investors who keep these four principles in mind are likely to dramatically outperform those who blindly follow the generic allocations recommended by many financial advisers... or worse, those who don't think about asset allocation at all.

Regards,

Porter Stansberry

Editor's note: Doc recently sat down with Porter at his farm where they discussed a major split happening in America right now. It's the beginning of a massive trend that will have an enormous impact on everyone and everything – including the financial markets.

Porter also shared the most critical step to take now to protect and grow your wealth in the unpredictable times ahead.

You can watch their full interview here.