Major announcement regarding Stansberry Asset Management...

Major announcement regarding Stansberry Asset Management... An update on the 'lions'... Why we believe stocks (yes, stocks) are the best way to protect your assets even during bear markets... How to get big profits from super-safe stocks (like McDonald's)...

![]() There's an important announcement regarding the formation of Stansberry Asset Management at the end of today's Digest. I urge all subscribers to read it carefully. If you have any questions about what's happening, please don't hesitate to ask me personally. Send a note to feedback@stansberryresearch.com. Remember, I personally read all of the e-mails that go to that address.

There's an important announcement regarding the formation of Stansberry Asset Management at the end of today's Digest. I urge all subscribers to read it carefully. If you have any questions about what's happening, please don't hesitate to ask me personally. Send a note to feedback@stansberryresearch.com. Remember, I personally read all of the e-mails that go to that address.

![]() But before we discuss anything else, I want to update you on the "lions" I warned about last month. I was concerned about a bear market developing in U.S. stocks because bear markets had already developed in emerging-market stocks. Likewise, prices of corporate bonds were falling, mostly because of weakness in the price of oil. And most worrisome of all, the Dow Jones Transportation Average Index was well into a correction. As I explained...

But before we discuss anything else, I want to update you on the "lions" I warned about last month. I was concerned about a bear market developing in U.S. stocks because bear markets had already developed in emerging-market stocks. Likewise, prices of corporate bonds were falling, mostly because of weakness in the price of oil. And most worrisome of all, the Dow Jones Transportation Average Index was well into a correction. As I explained...

At the very least, before I become bullish on U.S. stocks, I want to see these "lions" – emerging-market stocks, U.S. oil companies, U.S. transports, and the high-yield corporate-bond market – stabilize. As long as these critical pieces of the global economy remain in significant downtrends, there's no way U.S. stocks can sustain a rebound.

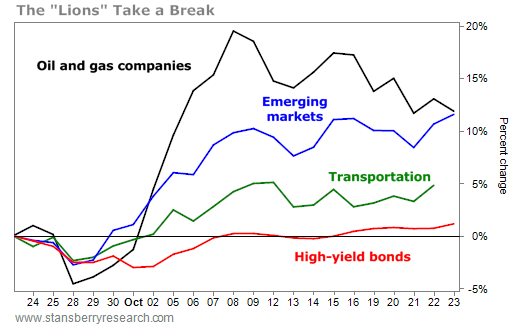

![]() On September 28, the "lions" retested the lows they set in late August and bounced higher. Here's a chart of the last 30 days, showing the relative performance of several funds and indexes focused on these sectors: oil and gas stocks (FRAK, up around 11%), emerging-market stocks (EEM, up around 11%), and the Dow Jones Transportation Average Index (DJT, up 5%). Notice, however, that U.S. corporate bonds (HYG, up 1%) have barely budged...

On September 28, the "lions" retested the lows they set in late August and bounced higher. Here's a chart of the last 30 days, showing the relative performance of several funds and indexes focused on these sectors: oil and gas stocks (FRAK, up around 11%), emerging-market stocks (EEM, up around 11%), and the Dow Jones Transportation Average Index (DJT, up 5%). Notice, however, that U.S. corporate bonds (HYG, up 1%) have barely budged...

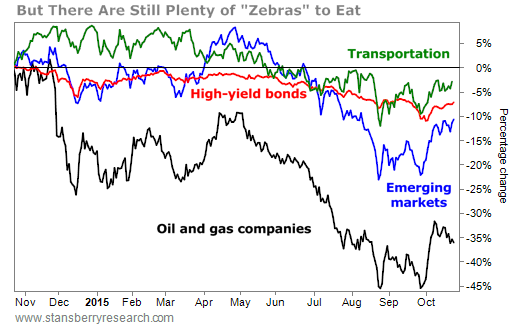

![]() It's good news that these funds and indexes are not still falling. It could be the first sign of stability in these markets, something that would be bullish for U.S. stocks. But I don't think we're out of the woods yet. A longer-term look at these same areas of the market shows how much "technical" damage has been done. In my view, none of these trends has truly "broken out." Look at a one-year chart of the same indexes and you'll see what I mean...

It's good news that these funds and indexes are not still falling. It could be the first sign of stability in these markets, something that would be bullish for U.S. stocks. But I don't think we're out of the woods yet. A longer-term look at these same areas of the market shows how much "technical" damage has been done. In my view, none of these trends has truly "broken out." Look at a one-year chart of the same indexes and you'll see what I mean...

![]() In my opinion, the single most important "lion" to watch is the U.S. corporate debt market, represented by the iShares High Yield Corporate Bond Fund (HYG). Over the last year it's still down around 7%. A negative return is unusual for the corporate-bond market, especially when there isn't a recession.

In my opinion, the single most important "lion" to watch is the U.S. corporate debt market, represented by the iShares High Yield Corporate Bond Fund (HYG). Over the last year it's still down around 7%. A negative return is unusual for the corporate-bond market, especially when there isn't a recession.

So far this year, 297 U.S. corporations have seen their bonds downgraded. That's the most downgrades in a year since the financial crisis of 2008-2009. The year isn't over yet. Neither are the downgrades. More worrisome, the 12-month default rate on high-yield corporate debt has doubled this year. This suggests we are well into the next major debt-default cycle.

![]() As I've been writing and warning for a long time, the coming debt default cycle will almost surely be a "super" cycle – meaning it will last longer and cause far more losses than most people expect.

As I've been writing and warning for a long time, the coming debt default cycle will almost surely be a "super" cycle – meaning it will last longer and cause far more losses than most people expect.

Historically, there's a six- to eight-year cycle during which credit builds. These periods are normally followed by a two- to four-year default cycle, during which credit tightens, making it impossible for weaker businesses to "roll" forward their debts by borrowing more money. That leads to rising defaults. When companies can't pay back their bondholders, they either go into bankruptcy, or they work out a private agreement in which debt is swapped for equity. The former lenders become the new owners.

![]() These default cycles are usually accompanied by a recession in the economy and a correction or a bear market in stocks. It seems highly likely that we've begun the credit-default cycle. And I think it's going to be a big one. Why? Over the last six years, lending terms were the "loosest" they have ever been. More money was lent to more companies, on more generous terms, than ever before. That by itself would normally create a more severe default cycle. But... there's a bigger problem this time.

These default cycles are usually accompanied by a recession in the economy and a correction or a bear market in stocks. It seems highly likely that we've begun the credit-default cycle. And I think it's going to be a big one. Why? Over the last six years, lending terms were the "loosest" they have ever been. More money was lent to more companies, on more generous terms, than ever before. That by itself would normally create a more severe default cycle. But... there's a bigger problem this time.

The last credit default cycle was cut short. Remember back in 2009 when the U.S. government supported the entire corporate-bond market through a huge smorgasbord of credit guarantees? That interrupted the last default cycle. In a normal credit-default cycle, between 25% and 40% of outstanding high-yield corporate bonds default over a period of two to four years.

But the last cycle lasted less than a year. It saw less than 2% of the outstanding issues default – all thanks to Uncle Sam's generosity. Taxpayers didn't get a thank-you note. And really, the government didn't do investors any favors, because all of those bad debts were merely "rolled forward." They're all still there.

That's the main reason experts (like Marty Fridson), analysts (like me), and major investors (like Carl Icahn) believe the next credit cycle will be a "doozy." Or as I like to call it: The greatest legal exchange of wealth in history.

Over the next 24 to 36 months, investors who buy the right distressed bonds at the right prices will end up owning trillions in high-quality assets. Lenders will become owners. And that's a trade I'll be helping investors make with a new product we're launching next month, Stansberry's Credit Opportunities. Keep an eye out for information about it.

![]() As long as U.S. corporate debt remains in a downtrend – which you can monitor by watching HYG shares – I don't think these lions will be able to sustain their uptrends. That's why I'm skeptical that the recent moves up will last. I still think we're heading into a bear market. If that's true, you might wonder why I don't sell all of the stocks in my model portfolio. You might wonder why I don't short dozens of stocks. The answer is: Because the timing on all these things is impossible to pinpoint and, because – and this is harder to understand – many of the stocks in our portfolio will perform well despite a bear market.

As long as U.S. corporate debt remains in a downtrend – which you can monitor by watching HYG shares – I don't think these lions will be able to sustain their uptrends. That's why I'm skeptical that the recent moves up will last. I still think we're heading into a bear market. If that's true, you might wonder why I don't sell all of the stocks in my model portfolio. You might wonder why I don't short dozens of stocks. The answer is: Because the timing on all these things is impossible to pinpoint and, because – and this is harder to understand – many of the stocks in our portfolio will perform well despite a bear market.

Look at McDonald's (MCD), for example. Yesterday, the stock soared – as we told subscribers it would. I invite you to go back and read our most recent recommendation – in the April 10 Digest. I explained in detail why most investors don't understand how capital efficient McDonald's is and how it's therefore able to support its investors through large dividends and share buybacks. Since then, the Dow Jones Industrial Average is down 3%. McDonald's is up 14%. I don't want to sell a great business that is paying us dividends and is sure to survive the next bear market... whenever it arrives.

![]() Most people don't believe me when I try to explain why bear markets are great for investors. To understand why we believe that certain stocks are the best hedge against tough times – better than gold, bonds, and real estate – I urge you to go back and read our recommendations of homebuilder NVR and famed chocolate maker Hershey.

Most people don't believe me when I try to explain why bear markets are great for investors. To understand why we believe that certain stocks are the best hedge against tough times – better than gold, bonds, and real estate – I urge you to go back and read our recommendations of homebuilder NVR and famed chocolate maker Hershey.

NVR is the only major homebuilder with a capital-efficient business model. It was profitable through the housing crisis and its stock has soared since (from around $400 per share to more than $1,600). Even if you had bought this stock at the very worst time, at the peak of the housing bubble in 2005, you would have still doubled your money in 10 years. And if you were wise enough to buy it when the market crashed in 2009, you could have made 300%, safely, over the last few years.

Likewise, we first recommended Hershey in December 2007 – just about the worst time imaginable to buy U.S. stocks. We're well on our way to earning more than 200% in that very safe investment. These profits will continue to grow, over time, thanks to growth in Hershey's dividends. These kinds of businesses are where you want to keep most of your savings. And bear markets are the best times to add to your collection.

![]() So no... we aren't going to panic and sell everything in our portfolio. We are going to take some profits (which we started doing in 2013). We are going to raise cash when we hit trailing stop losses. And we are going to add short positions to (hopefully) hedge against volatility in the overall market. But most of all, we're going to wait and watch the market patiently. We know a once-in-a-decade opportunity is building in the bond market. We're going to be very prepared for it.

So no... we aren't going to panic and sell everything in our portfolio. We are going to take some profits (which we started doing in 2013). We are going to raise cash when we hit trailing stop losses. And we are going to add short positions to (hopefully) hedge against volatility in the overall market. But most of all, we're going to wait and watch the market patiently. We know a once-in-a-decade opportunity is building in the bond market. We're going to be very prepared for it.

![]()

Announcing the Formation of Stansberry Asset Management

Dear subscribers,

Last week, at the annual Alliance meeting, Erez Kalir announced the formation of a new asset-management business, Stansberry Asset Management.

I (Porter Stansberry) wanted to take a moment to tell you about what this means for our publishing company and how it might affect you as a subscriber.

First, what's happening?

Well... in one way... nothing is changing. Our publishing company will continue to operate as it has for many years. It will still be headquartered in Baltimore. It will still be run by our CEO Matt Smith. And I will continue to play an active role in the business as the chairman of our board and one of the leading (hopefully) writers at Stansberry Research.

But we're also doing something completely new... something that I wasn't sure we would ever be able to do... and something that could be very risky for us...

We've decided to entrust the Stansberry name to Stansberry Asset Management and endorse a world-class investment manager, Erez Kalir.

Stansberry Asset Management ("SAM") will be a new registered investment-advisory firm that will offer managed accounts to high-net-worth investors. It will utilize investment research published by Stansberry Research. But Stansberry Asset Management will have no special or early access to our work. Erez and his team will receive information from Stansberry Research just like any other subscriber does – after the issues are published. Likewise, no one at Stansberry Research will have input or control over the day-to-day management of Stansberry Asset Management. The two companies will be completely separate.

However, Stansberry Asset Management will receive my full endorsement – so much so that I will be investing my own money with SAM as a client. Erez and his team will manage all of my stock investments – outside of a small Fidelity 401(k) – at his firm once it is ready to manage client assets. Stansberry Asset Management will manage my children's trusts, too.

I'm excited about this opportunity because I know thousands of my subscribers are looking for more help with their own portfolios – help that Stansberry Research is not licensed or equipped to provide.

I've gotten thousands of letters from subscribers who say we've educated them so much about investing that they can't go back to their regular brokers. But no matter how hard they try, they can't seem to do it all on their own. Whether it's a lack of discipline with trailing-stop losses... or a tendency to not diversify enough... or not having enough time to focus on their investments and missing great opportunities as a result... it can be impossible for some people with busy careers and families to manage a portfolio. These subscribers don't understand why we can't simply do it for them.

The reasons are complicated. But the quick answer is that we are not an investment adviser. We are a publisher and a research company. Money management is a completely different business that requires far more regulatory expertise and customer service.

It has been very difficult (and has taken a long time) to find someone to entrust with the Stansberry name, someone I knew was an outstanding investor in his own right. I didn't want to endorse anyone I wouldn't trust to manage my own money... and I didn't want to put my own investments in anyone else's hands unless I believed he was a better investor than I am.

When I met Erez, I knew I had found the right guy. In my view, he is one of the finest money managers of his generation. When I met him, he was running a hedge fund for renowned investor Julian Robertson. Tiger Management, Julian Robertson's family of hedge funds, is one of the largest and most prestigious asset-management firms in the world. At its peak, Erez's hedge fund controlled nearly $1 billion in assets.

As you can imagine, before I entrusted my name to any money-management firm, I wanted to be sure that I could fully endorse it. Erez and I have spent countless hours going over the philosophy and business approach that will guide his leadership of Stansberry Asset Management. I believe Erez has devised a far friendlier, fairer model than the typical hedge fund... one that does a better job of aligning incentives and gives investors who are focused on the long term the kind of treatment they deserve.

I can't be more excited about Erez's new business. As I told the audience last week, "Erez is as smart as I think I am." He graduated from Stanford with highest honors. Then he studied at Oxford as a Rhodes Scholar. He went on to Yale Law School and was on the law review there.

Erez followed up his education with an exemplary career – including stints managing money for some of the most well-known investors and endowments in America. His resume and list of mentors is a "who's who" of modern finance. In short, Erez is exceptionally well-qualified to lead this business. He's the only person in the entire world whom I trust and respect enough to give control over my personal investments in stocks.

And on top of that, I am confident Erez understands the investment principles that we believe in at Stansberry Research. He is a longtime subscriber and has been a Stansberry Research Alliance member for more than seven years. He has been reading the same newsletters that you read from Stansberry Research, and he'll continue to do this in his new venture.

There is a big risk for us at Stansberry Research, though. If subscribers think (or just fear) that Erez's team is able to access our ideas before other subscribers, then our reputation could be seriously damaged. That's why it's very important for you to understand that the two businesses are legally, physically, and operationally separate. One is located in Baltimore, and the other will be in New York City. They have different managers. They have different employees. They are in different businesses.

Erez and his team will not have any early or otherwise privileged access to the investment research or published products at Stansberry Research. They will receive our newsletters and e-mails just like any other subscriber does.

I think this is a great opportunity for people who appreciate the work produced by Stansberry Research but don't have enough time to read all of the content and manage their own investments... or people who struggle each year to get the results they're looking for. It's also a good diversification option for people who enjoy managing one area of their investments – like options or commodities – but who prefer to have other parts of their portfolio managed for them by a money manager who shares our philosophy, like Erez.

Erez's mission for his team at Stansberry Asset Management is to take Stansberry Research's investment ideas and combine them with asset-allocation, portfolio-construction, and risk-management tools typically reserved for institutional investors. SAM will also provide its clients access to niche asset classes – such as distressed residential mortgage notes or timber – that are ordinarily difficult for individuals to invest in on their own. And SAM will do all this while working hard to avoid many "Wall Street" money-management pitfalls – including packaged products, hidden fees, and simplistic stock-and-bond asset allocations based on criteria such as your age.

SAM is not for everybody, though. It's designed for portfolios of $500,000 or more.

Stansberry Asset Management aims to begin managing client assets in January 2016 and is currently accepting inquiries from investors. If you're interested in investing alongside me with SAM or would simply like to learn more, go to www.stansberryam.com for more information, including a copy of a detailed presentation about SAM that Erez shared at the Alliance conference.

Important note: Stansberry Research is a subscription-based publisher of financial information. Stansberry Research is not regulated by the U.S. Securities and Exchange Commission because it is a publisher. Stansberry Research and SAM are overseen by different boards and will be operated separately by different management teams.

SAM's management team is responsible for the investment decisions of SAM. The members of SAM's management team are not officers or editors of Stansberry Research and have no financial interest in Stansberry Research.

Porter Stansberry and the other writers at Stansberry Research are not personally involved in the day-to-day management of SAM or its investment advisory services, but some of them may choose to invest with SAM as clients.

Although SAM will utilize investment research published by Stansberry Research, SAM has no special or early access to such research. It receives information from Stansberry Research just like any other subscriber does – after the issues are published.

A solicitation arrangement exists under which Stansberry Research will be compensated by SAM to use the "Stansberry" name, to market to Stansberry Research subscribers, and should subscribers enter into investment-advisory relationships with SAM. Additional information about this arrangement and Stansberry Research will be furnished if you request additional information about SAM.

![]()

![]() New 52-week highs (as of 10/22/15): Activision Blizzard (ATVI), Chubb (CB), Expeditors International (EXPD), National Beverage (FIZZ), McDonald's (MCD), Altria (MO), Constellation Brands (STZ), Sysco (SYY), and Travelers (TRV).

New 52-week highs (as of 10/22/15): Activision Blizzard (ATVI), Chubb (CB), Expeditors International (EXPD), National Beverage (FIZZ), McDonald's (MCD), Altria (MO), Constellation Brands (STZ), Sysco (SYY), and Travelers (TRV).

Regards,

Porter Stansberry

Baltimore, Maryland

October 23, 2015

|