An update to our ETF portfolio...

An update to our ETF portfolio... Course correction... A portfolio for people who don't want to be investors... Why insurance will help your results... Reader feedback: How to add leverage to your portfolio...

![]() As longtime readers know, I'm a firm believer in always checking good intentions against actual results. I do this in many areas of my life – not just business and not just investing. Just think about how many times you've said something to yourself like, "I've always wanted to go to Paris." Fine. Anything (or almost anything) is possible if you track your intentions against your results. And we're going to do that today in regards to some advice I offered in the Digest about one year ago...

As longtime readers know, I'm a firm believer in always checking good intentions against actual results. I do this in many areas of my life – not just business and not just investing. Just think about how many times you've said something to yourself like, "I've always wanted to go to Paris." Fine. Anything (or almost anything) is possible if you track your intentions against your results. And we're going to do that today in regards to some advice I offered in the Digest about one year ago...

![]() Last year, I wrote a nine-essay series of Digests about the greatest investment secrets I had learned over the years. These essays weren't like the series I just completed last week. They weren't merely about finding good individual investments in the stock market. They were broader in scope. For example, the first thing I wanted to show our subscribers was a foolproof way to build a high-quality, diversified portfolio of exchange-traded funds (ETFs) – while paying almost nothing in fees...

Last year, I wrote a nine-essay series of Digests about the greatest investment secrets I had learned over the years. These essays weren't like the series I just completed last week. They weren't merely about finding good individual investments in the stock market. They were broader in scope. For example, the first thing I wanted to show our subscribers was a foolproof way to build a high-quality, diversified portfolio of exchange-traded funds (ETFs) – while paying almost nothing in fees...

I'm going to give you seven well-run ETFs that you can buy safely and enjoy their outstanding investment performance... even if you know absolutely nothing about investing and you have no desire to learn. This is for all of our readers who don't want to manage their own assets, but want better-than-reasonable returns on their savings...

What we're looking for in our list of the seven best ETFs isn't necessarily diversification or the cheapest possible fees, we're looking for funds that help investors succeed. We're looking for funds that are based on solid financial research and follow strategies that make sense to us.

![]() We recommended these seven ETFs. One (BXMT) is technically an investment company, but it performs the same function as an ETF. Their symbols and their performance, including dividends, over the last year is noted in parentheses...

We recommended these seven ETFs. One (BXMT) is technically an investment company, but it performs the same function as an ETF. Their symbols and their performance, including dividends, over the last year is noted in parentheses...

| • | Cambria Shareholder Yield Fund (SYLD, +8.2%) |

| • | WisdomTree Emerging Markets Equity Income Fund (DEM, -10.4%) |

| • | United States Commodity Index Fund (USCI, -23.6%) |

| • | Blackstone Mortgage Trust (BMXT, +6.8%) |

| • | Market Vectors Unconventional Oil & Gas Fund (FRAK, -35.9%) |

| • | PowerShares International Dividend Achievers Portfolio (PID, -5.0%) |

| • | SPDR Dow Jones International Real Estate Fund (RWX, -1.7%) |

The overall return on our ETF portfolio, including dividends, was -8.3%.

Meanwhile, the benchmark S&P 500 Index was up 10.6% with dividends included. Another comparison we made, a simple basket of four big and cheap-to-own mutual funds (domestic and foreign) was up 5%. In short, passive investors would have done far better over the last year by investing either in a U.S. index fund (which you can own with almost no overhead expense) or even a basket of mutual funds.

Also, interestingly, active investing has done much better over the past year, thanks to some large moves in commodity prices. My Investment Advisory portfolio recommendations, for example, are up 20% over the past year on an annualized basis, roughly double the market's average return.

![]() What happened? Why did our ETF portfolio underperform similar investment vehicles so badly?

What happened? Why did our ETF portfolio underperform similar investment vehicles so badly?

In retrospect, there is one glaring problem with the ETF portfolio I recommended: It's far too heavily weighted toward commodities. Out of the seven positions in our ETF portfolio, four are commodity related: real estate, oil and gas, commodity futures index, and emerging markets (which are highly correlated to commodities).

This portfolio allocation weakness became clear as the U.S. dollar rallied over the last year and as oil prices plunged. Both factors – the strong dollar and falling oil prices – are the reason why this portfolio lost money and badly lagged the performance of U.S. stocks.

![]() Does this mean our idea is flawed? I don't think so. We could easily fix this portfolio. Even though commodities performed poorly, in many ways, our portfolio functioned as we intended. We picked these particular ETFs because we admired the way they were constructed.

Does this mean our idea is flawed? I don't think so. We could easily fix this portfolio. Even though commodities performed poorly, in many ways, our portfolio functioned as we intended. We picked these particular ETFs because we admired the way they were constructed.

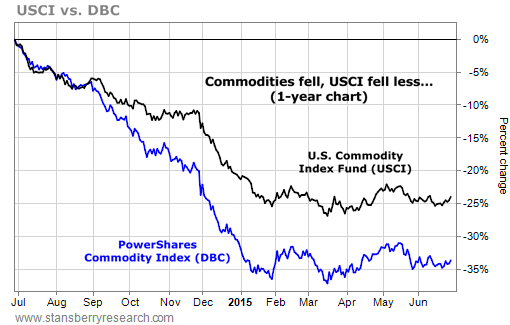

Take our commodity futures ETF, the U.S. Commodity Index Fund (USCI). This ETF is unique. It only owns commodity futures contracts where they're not trading in a "contango" pattern. (A market is in contango when delivery prices must converge downward to meet futures prices. Obviously, you don't want too own a commodity whose price is going to fall.) Likewise, this fund uses a simple trend-following strategy to stay out of commodities that are in a nosedive. These factors helped to greatly mitigate our losses as commodities collapsed over the last year and as oil prices have remained in contango.

Here's how USCI fared against the largest ETF of its kind, the PowerShares DB Commodity Index Tracking Fund (DBC)...

![]() Looking carefully at our results so far, rather than abandoning the idea, we simply need to make a minor course correction. We need to reduce our exposure to commodities. The obvious choice is to remove the oil frackers fund (FRAK). These stocks are going to be volatile and, over the long term, as a group, are unlikely to beat the market as a whole.

Looking carefully at our results so far, rather than abandoning the idea, we simply need to make a minor course correction. We need to reduce our exposure to commodities. The obvious choice is to remove the oil frackers fund (FRAK). These stocks are going to be volatile and, over the long term, as a group, are unlikely to beat the market as a whole.

That's a bad combination when you're trying to build a low-risk, diversified portfolio of ETFs. I made a poor choice by including it originally. I was too bullish on U.S. shale oil and not cautious enough about how booming U.S. production would eventually hurt oil prices and oil profits. That's the big problem with commodities – good news leads to bad news.

![]() By removing the direct trade on oil, we don't lose our exposure to oil – we'll get that in our commodity index fund. Likewise, we'll continue to have plenty of U.S. dollar hedges, via global real estate, global dividend-paying stocks, and emerging-market stocks. And adding an insurance ETF will give us something important for our portfolio: a low-volatility way to beat the market.

By removing the direct trade on oil, we don't lose our exposure to oil – we'll get that in our commodity index fund. Likewise, we'll continue to have plenty of U.S. dollar hedges, via global real estate, global dividend-paying stocks, and emerging-market stocks. And adding an insurance ETF will give us something important for our portfolio: a low-volatility way to beat the market.

![]() There's only one insurance ETF that specifically doesn't own life insurance companies. It's the PowerShares KBW Property & Casualty Insurance Fund (KBWP). We greatly prefer the property and casualty insurance business to the life insurance business because everyone dies. But not everyone wrecks their car or files a homeowners' insurance claim. As a result, property and casualty companies with excellent underwriting discipline can be outstanding investments, far better than life insurance companies.

There's only one insurance ETF that specifically doesn't own life insurance companies. It's the PowerShares KBW Property & Casualty Insurance Fund (KBWP). We greatly prefer the property and casualty insurance business to the life insurance business because everyone dies. But not everyone wrecks their car or files a homeowners' insurance claim. As a result, property and casualty companies with excellent underwriting discipline can be outstanding investments, far better than life insurance companies.

![]() We've written about these advantages for investors time and time again since 2012. I encourage you to consider building your own basket of property and casualty insurance stocks using our work. You can find our highest-ranked insurance companies by using our Insurance Monitor, which is part of our supplementary Stansberry Data publication.

We've written about these advantages for investors time and time again since 2012. I encourage you to consider building your own basket of property and casualty insurance stocks using our work. You can find our highest-ranked insurance companies by using our Insurance Monitor, which is part of our supplementary Stansberry Data publication.

I specifically didn't include this insurance fund last year because I believe we'll do a better job in my newsletter picking insurance stocks than this ETF will do for you. But that's missing the point. This ETF portfolio isn't for people who want to manage their own money. This is for people who specifically don't want to deal with buying individual stocks.

![]() Adding insurance to our ETF portfolio does something else for us, too. It lowers volatility. High-quality insurance stocks produce slow and steady gains. The PowerShares property and casualty fund is about 10% less volatile than the overall S&P 500. That means when stocks fall, this fund tends to fall less. Likewise, when the market has a big up day, these stocks typically don't jump as much.

Adding insurance to our ETF portfolio does something else for us, too. It lowers volatility. High-quality insurance stocks produce slow and steady gains. The PowerShares property and casualty fund is about 10% less volatile than the overall S&P 500. That means when stocks fall, this fund tends to fall less. Likewise, when the market has a big up day, these stocks typically don't jump as much.

Meanwhile, the annual returns (up 16.6% over the last year) are likely to continue beating the market. Another one of our recommended investments, the Blackstone Mortgage Trust, has super-low volatility – it's about half as volatile as the market as a whole. In my experience, investors tend to overestimate their own risk tolerance. Having low- and super-low-volatility positions is the key to building a portfolio most investors can live with happily.

![]() If we indulge in a bit of 20/20 hindsight investing, we find that replacing oil stocks (FRAK) with insurance stocks (KBWP) would have caused our portfolio to break even over the last year (-0.8%) rather than losing 8.3%. We still would have underperformed U.S. stocks (+10.6%) on average, and we would have still underperformed a basket of U.S. and international stock mutual funds (+5%).

If we indulge in a bit of 20/20 hindsight investing, we find that replacing oil stocks (FRAK) with insurance stocks (KBWP) would have caused our portfolio to break even over the last year (-0.8%) rather than losing 8.3%. We still would have underperformed U.S. stocks (+10.6%) on average, and we would have still underperformed a basket of U.S. and international stock mutual funds (+5%).

With the kind of exposure we have to emerging markets and commodities, that's the price we're going to pay when the dollar has a big rally and commodities fall out of bed. For us, breaking even in a year like this sets up future outperformance. I know this portfolio will beat U.S. stocks by a wide margin when the dollar is flat or weakening. And if you know much about the history of the U.S. dollar, you know that's what happens most of the time.

![]() One final point... If you recall my advice from last year, I said if you allocate additional savings to this basket of ETFs each year – buying those that are down the most – you'll end up doing well over the long term. I still believe that's true. This portfolio is designed to beat the market over any reasonable period of time, which in my book is anything longer than five years. If you're disciplined enough to buy parts of the portfolio when they're down, I'm certain you can significantly add to your total returns over time.

One final point... If you recall my advice from last year, I said if you allocate additional savings to this basket of ETFs each year – buying those that are down the most – you'll end up doing well over the long term. I still believe that's true. This portfolio is designed to beat the market over any reasonable period of time, which in my book is anything longer than five years. If you're disciplined enough to buy parts of the portfolio when they're down, I'm certain you can significantly add to your total returns over time.

![]() New 52-week highs (as of 6/25/15): Dollar General (DG).

New 52-week highs (as of 6/25/15): Dollar General (DG).

![]() Porter answers a subscriber's question on adding leverage to your investment portfolio in today's mailbag. As always, send your queries to feedback@stansberryresearch.com.

Porter answers a subscriber's question on adding leverage to your investment portfolio in today's mailbag. As always, send your queries to feedback@stansberryresearch.com.

![]() "Hi Porter, please show an example of how you would add leverage to your capital efficient portfolio using just one real company and the results from the actions taken to leverage it, could be very instructive." – Paid-up subscriber Pat

"Hi Porter, please show an example of how you would add leverage to your capital efficient portfolio using just one real company and the results from the actions taken to leverage it, could be very instructive." – Paid-up subscriber Pat

Porter comment: Leverage simply means using borrowed capital. Borrowing money in excess of your portfolio's liquidation value (or "equity value") will increase the volatility of your returns for obvious reasons. When stocks go up, using borrowed money will increase the returns, as measured against the equity value of your portfolio. Likewise, when stocks fall, leverage will magnify your losses – whether paper or realized.

But most investors should never use leverage. In my experience, most investors have a hard enough time simply learning to make money in the stock market. Just think back to 2008-2009. Imagine what would have happened to you if you had borrowed 25% or 50% of the money you were investing. You probably would have seen your account fall all the way to zero. Thus, my advice: Don't do it.

On the other hand, for investors who are highly disciplined and attracted to our work in insurance, capital-efficient stocks, and "forever" blue chips, leverage is a reasonable way to increase your returns. Leverage is a way to maximize the "alpha" found using these safe strategies. Alpha is a finance-geek term that refers to the return generated by a portfolio per unit of risk, where risk is approximated by measuring volatility. As we have proven over many years, low-volatility portfolios like ours can generate total returns in excess of the average return in stocks. Ergo, using leverage to equalize portfolio volatility with the market as a whole may also lead to even larger outperformance, without adding risk in excess of the market's average volatility.

In short, if you can stand the average volatility of the stock market... and if you're knowledgeable enough to measure the risk in your own portfolio... and if you're disciplined... there's no reason not to add a little leverage into your portfolio and thereby increase your total returns.

Having said that, let me reiterate what I said first: While some investors might benefit from this approach, you shouldn't do this. This approach involves things like risk-parity position-sizing that are difficult for most people to manage. Likewise, this approach may add costs that erode or eliminate any total return gained. For example, currently only Interactive Brokers provides margin loans at reasonable rates. In every other case, what you'll spend borrowing the money will probably eat up all of the excess returns that are generated. Ameritrade, for example, charges an outrageous 9% on small accounts. Apply that rate against your average returns over the last 10 years and I'd bet you end up in the red. That's why I say most people shouldn't use margin. But if you do, definitely shop around – the interest rates on margin loans vary widely.

If this is all so hard to do and expensive, why would I bother writing about it at all?

One, I think it's an interesting and valuable approach. No doubt there are many sophisticated investors (and professional investors) reading who will benefit tremendously from using this kind of approach. Also, I'm currently in the process of building an investment-services business (Stansberry Asset Management) that plans to offer these services for investors. These kinds of approaches are what make it worth it to pay an investment manager. If your investment manager isn't currently doing these things, having this information may empower you to ask better questions about the service you're currently receiving.

On the other hand, if you're determined to do this on your own... let me tell you one more time: Don't do it. Using leverage will almost invariably get you in big trouble. Save yourself the heartache. At the very least, don't do it until you can accurately measure the risk of your existing portfolio. Don't do it until you can size your portfolio positions accurately by volatility.

Let's say your portfolio has the same "average" volatility of the stock market, but you achieved that by investing in one radically volatile, risky biotech stock and then adding six or so conservative, less volatile stocks, if you increase the positions equally using, say, 25% leverage in your portfolio, you could end up taking far more risk than you realize... because one of your positions is much more volatile than the others. In these situations, it's better to manage your position-sizing according to volatility rather than just weighing everything equally.

Dr. Richard Smith at TradeStops is building a set of tools that will help individual investors figure out how to do these things using their own portfolios. Within a few weeks, Richard tells me that TradeStops subscribers will be able to quickly measure the volatility of their existing portfolio to determine if it's prudent to consider adding leverage. Another new tool will show you how to position size for volatility to spread your risks evenly accord your entire portfolio.

Adding leverage from that point is simple. You just spread the borrowed money equally across your positions. Whatever you do, do not use leverage without these tools. If you don't subscribe to TradeStops, you're being pennywise and pound foolish. Stansberry Research invested in TradeStops because there's no better or easier way to manage trailing stops. But that's just the beginning of what Richard's software can teach you about position-sizing, risk management, and how to maximize your results. Everyone managing his own portfolio should use these tools.

Regards,

Porter Stansberry

Cockeysville, Maryland

June 26, 2015

|