The Chip King's Next Move

Editor's note: The AI boom made Nvidia the world's most valuable company. But its biggest opportunity may still lie ahead – despite what the market is expecting. Joel Litman, chief investment officer of our corporate affiliate Altimetry, explains why the company's latest push into an overlooked corner of AI infrastructure could create another powerful engine for long-term growth...

Also, our offices and the markets are closed tomorrow ahead of Independence Day, so our next issue of DailyWealth will publish on Monday, after the Weekend Edition. Enjoy the holiday!

If you've followed Jensen Huang this far, your patience has paid off...

Chip giant Nvidia (NVDA) spent decades proving graphics processing units ("GPUs") were useful for more than video games and visual rendering.

A GPU is built to do a huge number of similar calculations at the same time. That makes it perfect for training AI models... where systems chew through mountains of data and repeat mathematical operations over and over.

Nvidia's GPU chips became the workhorses of AI. They've helped train the AI models that are dominating the headlines this year. Shares are up roughly 1,100% since the launch of ChatGPT.

Huang isn't done, though. He's now looking backward... to the central processing unit ("CPU").

In a word, the market seems... underwhelmed. The question for us as investors is: should it be?

Nvidia Has Found Its Next Growth Engine

The world has considered CPUs far less exciting than GPUs for years...

CPUs are the "brains" of the computer. They handle broader, more complex tasks – and, typically, they complete those tasks one at a time. CPUs can manage instructions and coordinate the rest of the parts within a computer.

Training the biggest AI models, though, requires brute-force parallel processing – running simple calculations millions of times. You have to split up the work, simultaneously, over multiple processing cores.

Nvidia owned the training market through its top-of-the-line GPUs. It's what made the software giant the biggest company in the world.

But there are tons of AI models out there now. Training new ones isn't as important. And that brings Nvidia to the next logical challenge... using those models.

That means running agents and coordinating tools across millions of users. In that world, CPUs become more important.

In May, Nvidia launched Vera – a CPU designed for AI. Nvidia says Vera is twice as efficient and 50% faster than traditional CPUs. And the company announced that the AI-focused CPU was in full production.

Customers and partners already include Facebook owner Meta Platforms (META), software giant Oracle (ORCL), cloud-computing company CoreWeave (CRWV), and computer maker Dell Technologies (DELL).

The CPU market used to be a two-horse race... controlled by Advanced Micro Devices (AMD) and Intel (INTC). But based on what we're seeing, Nvidia isn't content to stay in its lane.

In short, Vera could be a huge growth opportunity for the biggest company on Earth...

Nvidia minted roughly $216 billion in revenue for fiscal 2026. Analyst consensus is for revenue to grow 32% per year to $861 billion in the next five years.

So Wall Street seems to understand how the CPU market could turbocharge revenue. But as it often does, the problem lies with investors...

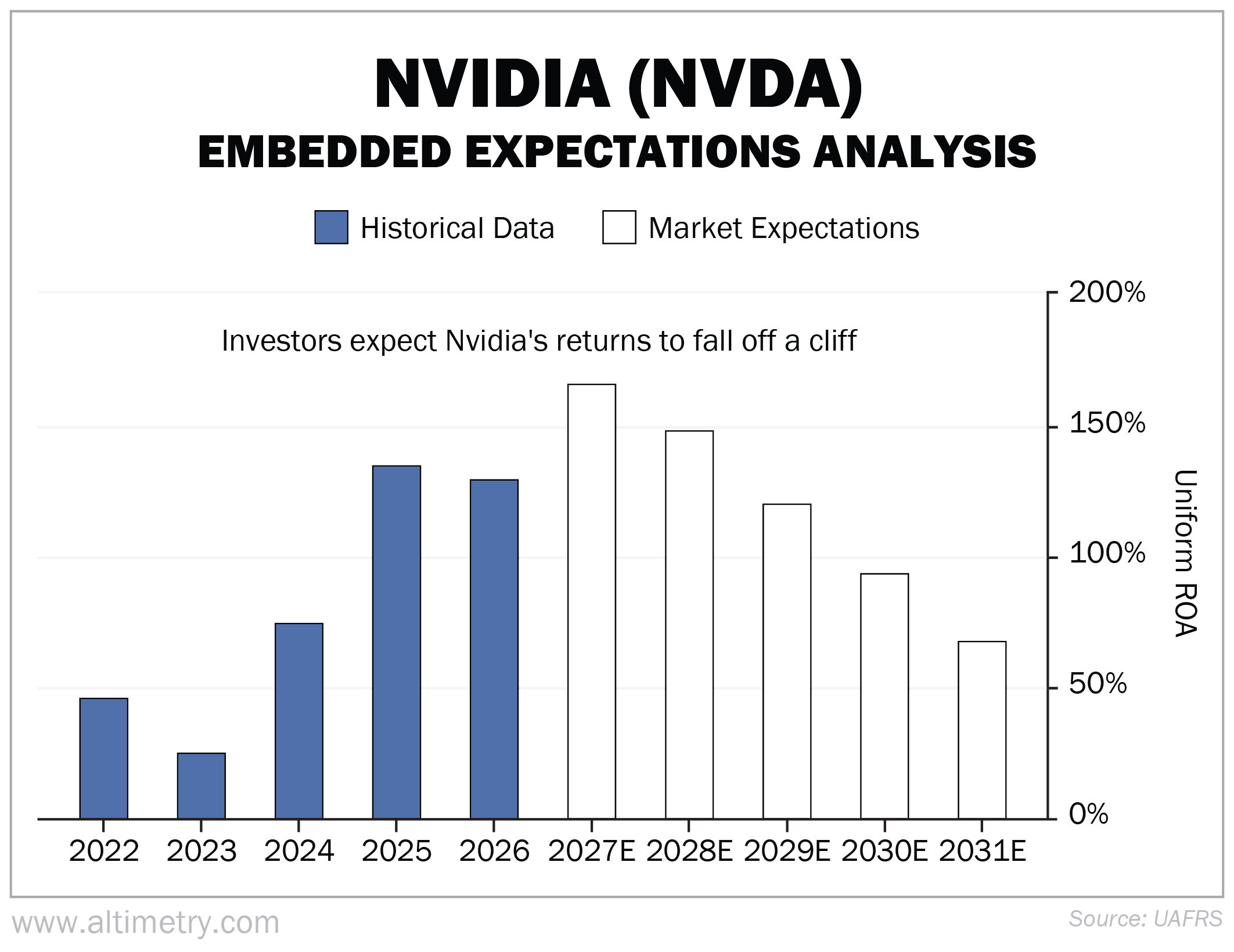

To get a sense of what the market is thinking, we turn to our Embedded Expectations Analysis ("EEA") framework – a staple for us at Altimetry.

The EEA works a lot like a betting line in a sports bet... We use Nvidia's current share price to calculate what investors expect from future performance and compare those forecasts with our own.

It tells us how well our "team" (the company) has to perform to justify the market's "bet" (the current price).

Let's assume Wall Street's estimate is accurate. If Nvidia's stock stays where it is right now, at roughly $207 per share... and assets grow 32% per year... we're looking at a Uniform return on assets ("ROA") around 68%.

That's a steep drop from last year's 129% returns. It's also lower than what Nvidia has generated in each of the past three years...

Much of the market is treating this business as though it will give up most of the profitability it has earned in the AI boom.

But Nvidia's GPU dominance created one of the most profitable supply bottlenecks in history...

AI hyperscalers had to go through Nvidia to run their models. There was no other option.

Now, the next great bottleneck could very well form around CPUs.

AMD and Intel have room to benefit here... And so does Nvidia. We expect it to keep expanding even after the GPU boom.

And if and when those folks are proved wrong on Nvidia, investors are in for some serious upside.

Regards,

Joel Litman

Editor's note: Global asset manager BlackRock believes a $23 trillion opportunity is taking shape in one overlooked corner of the market. That's why Joel recently teamed up with Landon Swan to find the companies at the center of the coming trend... And they've already identified a handful of companies that could become some of the biggest winners of AI's next chapter.

Further Reading

Bull markets rarely end when investors are still betting against them. Despite headline-making rallies that resemble mania, one key measure shows traders are deeply bearish on technology... a setup that has historically pointed to stronger returns ahead.

Everyone knows AI is fueling demand for semiconductors. What's easier to overlook is how chips are becoming essential across industries like healthcare, manufacturing, and transportation... creating multiple long-term growth drivers that extend well beyond today's AI boom.